How Thames Water’s Green Bond Crisis Tarnished a Market

- Green Finance Society

- Nov 22, 2024

- 3 min read

Corporate Green Bonds | Debt | Credibility

Thames Water has landed itself in hot water. The UK’s biggest freshwater supplier and third-largest corporate green bonds issuer has debt repayments and inflation stresses that have single-handedly blemished the UK’s green bond portfolio’s creditworthiness. Since 2018, these green bonds have been used to refinance existing sustainable projects, such as wastewater treatment and renewable energy.

A medley of factors has caused Thames Water’s green bonds to go down the drain. Their environmental record has been compromised by high pipeline leakage rates, high repair requests, and the release of millions of litres of sewage into rivers near Gatwick Airport. The latter had cost them £3.33 million and caused the death of over 1400 fish [1].

Along with ecological debacles, the company has repeatedly been deemed as a “powerful totem of mismanagement, corporate greed and lax regulatory oversight” [2]. Before being acquired by Macquarie in 2006, Thames Water was suspected to be syphoning off dividends and increasing debt [3]. Their performance under Macquarie from 2006-2017 only made things worse – Thames Water was £10bn in debt when they were sold by its parent company [4].

Since then, their dues have continued to mount and ultimately resulted in rating agencies such as Moody’s Ratings and S&P downgrading the company’s green bonds by five ranks [5]. As of September 2024, the company has warned that it could deplete its cash reserves by Christmas, earlier than anticipated, unless creditors grant access to £380 million in undrawn funds. This alarmed credit rating agencies, leading to a further downgrade and a "negative" outlook on its management, signalling to investors a heightened risk of default [6].

The Downfall of Thames Water’s Green Bond Creditworthiness

High pipeline leakage rates

High repair requests

Release of millions of litres of sewage into rivers

Penalty of £3.33 million

Syphoning off dividends

In a bid to mitigate their problems, Thames Water has structured its bond repayments to be dependent on customer bill cash flows instead of assets. This means that its ability to pay back its bonds is tied to the revenue generated from customers paying their water bills. Yet, this has only brought about low customer satisfaction, as elucidated in Ofwat’s 2021-22 performance report [7].

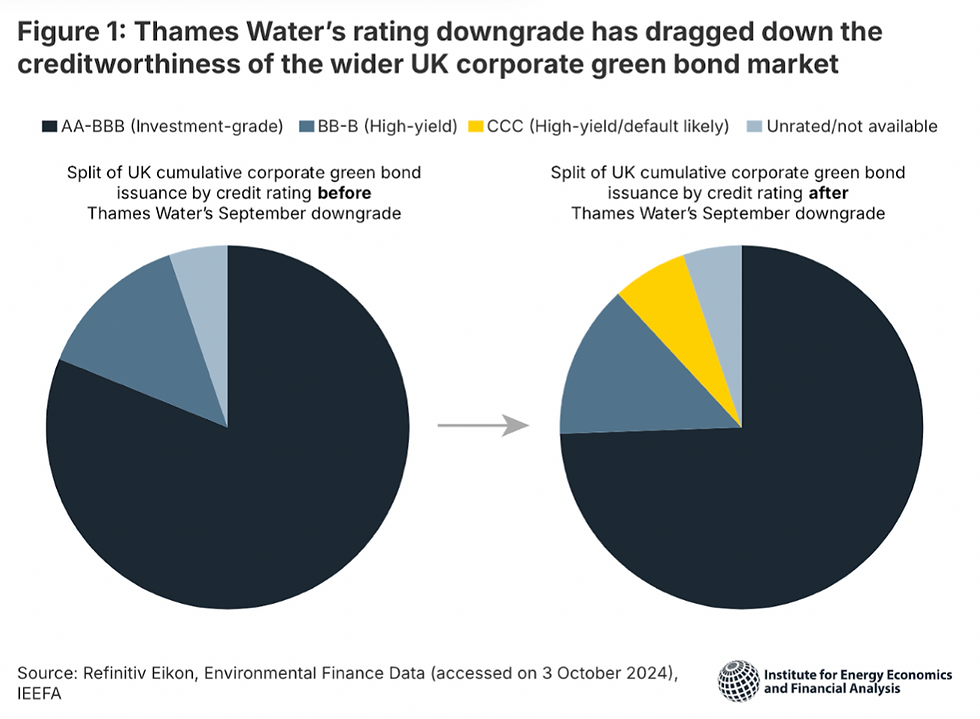

Before Thames Water’s downgrade in September, 92% of the UK's corporate green bond issuance was investment-grade (AA-BBB). The portfolio now comprises comparatively large proportions of CCC- and BB-B-rated bonds (see Figure 1) [8]. Green bond downgrades have impacted the creditworthiness of the green bond market as they deter future investors from the UK’s sustainable finance initiatives.

The degradation of Thames Water’s green bonds is an opportunity to reflect on the UK’s overarching sustainable financial strategy and evaluate its success. It is a reminder that simply labelling the bond as ‘green’ should not imply a singular focus on environmental benchmarks [9]. Thames Water proves how simply earmarking the funds for environmental purposes is insufficient in making a case for sustainable practices. Instead, a holistic approach incorporating all three elements of ESG—environment, social, and governance—is required. The trifecta ensures that crucial managerial and institutional factors that underpin the success of the green bond are addressed.

The success of a sustainable financial strategy also banks on the growth of the corporate green bond market which can further spur disclosure transparency and the adoption of sustainable business practices. Yet, it is important to remember that the credibility of bonds trumps their quantity, as we have learnt from Thames Water’s pitfalls. Hence, the development of more robust sustainable bond standards can improve the accuracy of assessments of green bonds. In turn, this can increase credibility, transparency and the steady growth of the corporate green bond market.

Research Analyst: Shreya Prasad

Research Editor: Victoria Lim

References:

[1] Johnathan Owen, “Thames Water - Green Is Not Always Clean,” Thames Water - Green is not always clean | Blog TwentyFour AM (TwentyFour Asset Management, July 6, 2023)

[2] Anna Isaac and Alex Lawson, “Debt, Sewage and Dividends: The Rising Tide of Thames Water’s Troubles,” The Guardian, July 11, 2024, sec. Business,

[3] Lawson, Alex, and Anna Isaac. 2024. “Thames Water Accused of ‘Chicanery’ over £150m Dividend Payment.” The Guardian. The Guardian. July 2024.

[4] King, D. J. & B. (2024, August 28). Why is thames water in so much trouble?. BBC News.

[5] Kar, Tuhin, and Giulia Morpurgo. 2024. “S&P Cuts Thames Water’s Top-Ranked Bonds to Junk.” Bloomberg.com. Bloomberg. July 31, 2024.

[6] Kelso, P. (2024, September 27). Uncomfortable truth is that Thames Water’s fate may be out of existing management’s hands. Sky News.

[7][9] Johnathan Owen, “Thames Water - Green Is Not Always Clean,” Thames Water - Green is not always clean | Blog TwentyFour AM (TwentyFour Asset Management, July 6, 2023)

[8] Kevin Leung, “Green Bonds down the Drain: What Thames Water’s Debt Crisis Could Mean for UK Sustainable Finance,” Ieefa.org, 2024

Comments